Inheritance of Digital and Cryptocurrency Assets in Israel – A Legal Perspective

By: Adv. David Melnik

In recent years, more and more Israelis hold digital assets – whether virtual currencies such as Bitcoin and Ethereum, NFT tokens, accounts on trading exchanges, or other types of blockchain-based assets. According to the State Comptroller's report of November 2024, it is estimated that over 200,000 holders of digital assets are active in Israel, with growing financial volumes.

However, the issue of inheriting these assets has not yet received explicit regulation in Israeli legislation. It raises legal, tax, and practical questions that anyone holding digital assets should be aware of when drafting their will and planning the transfer of wealth to the next generation.

Cryptocurrency Assets Pass by Inheritance

The Israeli Inheritance Law, 5725-1965, states in Section 1 that "upon a person's death, the estate passes to the heirs." The definition of "estate" includes all assets, rights, and obligations of the deceased. This definition is broad and inclusive – covering tangible assets such as real estate and chattels, intangible assets such as contractual rights, patents, and copyrights, as well as means of payment such as foreign currency. All of these pass to the heirs under a will or by law, regardless of their internal classification.

Cryptocurrency assets are included in the estate by virtue of this broad definition, independently of any classification debate. Whether classified as foreign currency or as an asset, they would pass to the heirs. The classification affects other matters – primarily the manner of taxation – but not the fact of inheritance itself.

The Kopel Ruling and Its Tax Implications for the Heir

The Central-Lod District Court ruled in the matter of Tax Appeal 11503-05-16 Noam Kopel v. Rehovot Assessing Officer (May 19, 2019) that Bitcoin is an "asset" for the purposes of Section 88 of the Income Tax Ordinance, and not a currency. The question in the ruling was whether a profit of over 8 million shekels that Kopel realized from selling Bitcoin was subject to capital gains tax, or whether it was exempt as "linkage differentials" applicable to foreign currency.

The court rejected the claim that Bitcoin is a currency and ruled that it is an asset whose sale constitutes a tax event. An appeal filed to the Supreme Court (Civil Appeal 5340/19) was withdrawn by agreement of the parties in 2022, making the ruling final and the precedent firmly established.

The implication of this ruling for crypto inheritance is not in the actual transfer to heirs (which derives anyway from the Inheritance Law), but rather in the tax burden that will apply to the heir upon realizing the assets. Because cryptocurrency is classified as an asset and not as currency, capital gains tax rules apply, and the gain is calculated as the difference between the sale price and the original purchase price. This issue will be discussed further in the article.

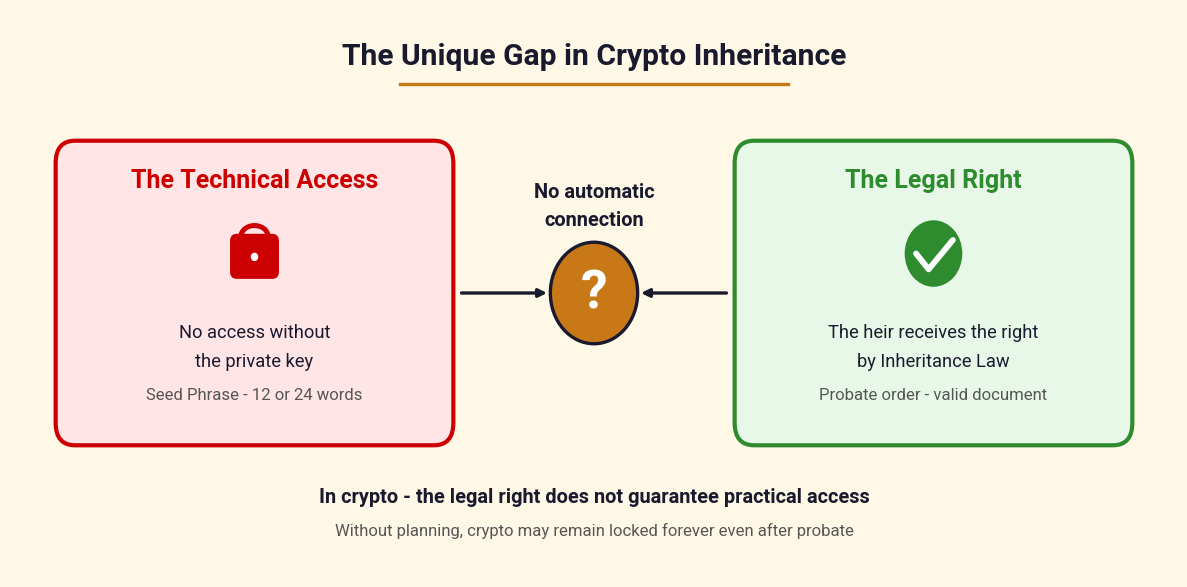

The Unique Gap – Between Legal Right and Technical Access

While the legal framework for crypto inheritance is clear, the unique challenge lies in the technical structure of these assets. Ownership of cryptocurrency is determined by possession of the private key – a cryptographic sequence typically protected by 12 or 24 words known as the "Seed Phrase" or "Recovery Phrase." Anyone holding the private key can transfer the asset to any address in the world.

This situation creates a practical gap that does not exist with other assets: even if a court issues a probate order or a grant of probate determining who the legal heirs of the cryptocurrency are, without access to the private keys, the legal right has no practical meaning.

For tangible assets and bank accounts, there is an intermediary – the Land Registry, the Real Estate Registrar, the bank – that is required to accept the probate order and act upon it. The right can be enforced through execution proceedings. In crypto, there is no such intermediary. The blockchain is a decentralized system, and there is no central authority that can enforce the transfer of assets pursuant to a court decision.

The consequence of this reality is that crypto inheritance planning requires not only legal arrangements through the will, but also practical arrangements for transferring the private keys to the heirs.

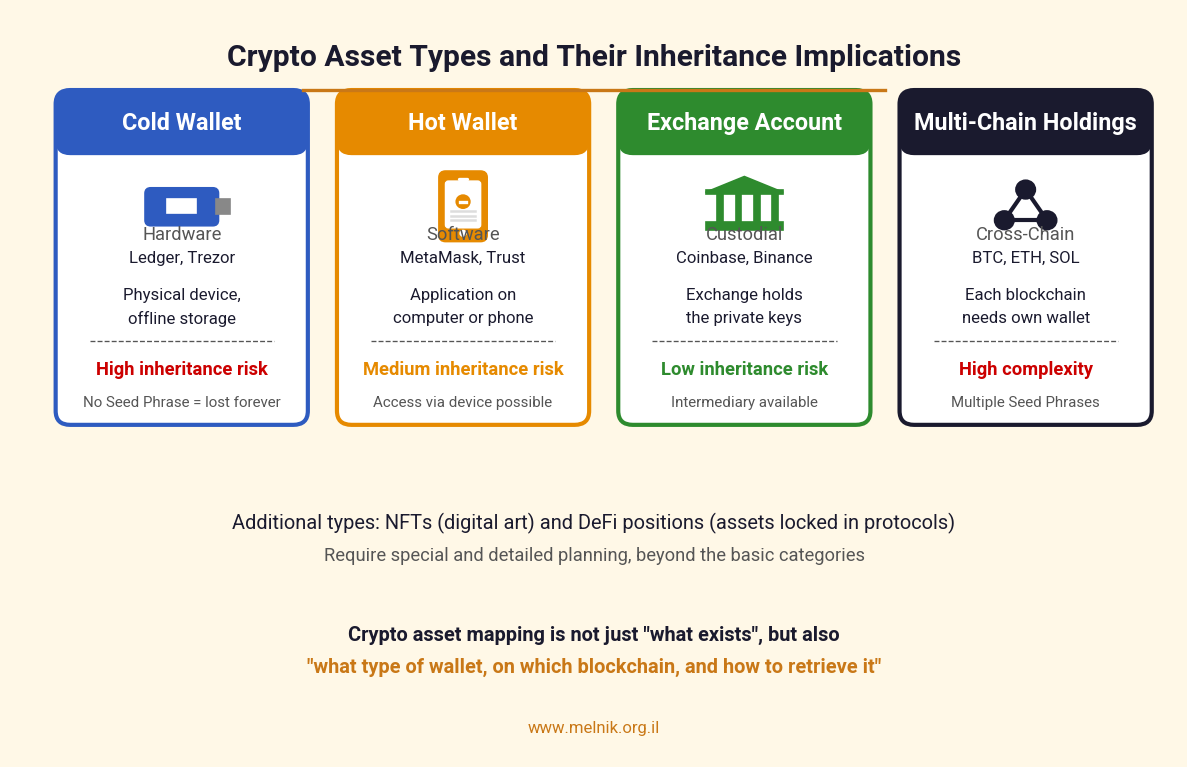

Different Asset Types and Their Inheritance Implications

The term "crypto assets" actually covers a wide range of assets that differ from one another in their technical characteristics and in the practical manner of their inheritance. Understanding the differences between asset types is essential for inheritance planning.

Cold Wallet. A physical device such as Ledger or Trezor, where private keys are stored offline. This is the most secure storage method against hacking, but also the most difficult to transfer through inheritance. Without knowledge of the Seed Phrase generated when the device was set up, heirs cannot access the assets even if the device itself is in their possession. In the extreme case, if the passphrase is lost and there is no backup, the cryptocurrency will remain on the blockchain forever without anyone being able to reach it.

Hot Wallet. An application or browser extension such as MetaMask, Trust Wallet, or Phantom, stored on the holder's computer or mobile phone and connected to the internet. Here too, there is dependence on the Seed Phrase, and additionally the wallet is exposed to cyber risks during the holder's lifetime. In terms of inheritance, if heirs gain access to the deceased's computer or phone with the appropriate password, there is a better chance of locating the cryptocurrency compared to a hidden cold wallet.

Exchange Accounts (Custodial Wallets). Accounts at trading exchanges such as Coinbase, Binance, Kraken (foreign), or Bits of Gold and Bit2C (Israeli). Unlike private wallets, here the exchange actually holds the private keys, and the customer connects to the account through a username and password. From an inheritance perspective, this is the relatively easier situation – there is an institutional intermediary that can be approached with a probate order. However, the process may be long and complex, especially with foreign exchanges, and requires documents translated and notarized, sometimes also with an Apostille. The release process at foreign exchanges typically takes 30 to 90 days, and sometimes longer.

Multiple Blockchains and Multi-Token Holdings. Every virtual currency resides on a specific blockchain – Bitcoin on its own blockchain, Ethereum on its, Solana, and so on. Each blockchain requires its own compatible wallet. A holder with five coins across five different blockchains may have five different wallets, each with its own Seed Phrase. This aspect increases the complexity of planning – heirs need to know not only where the cryptocurrency is located, but also which wallet corresponds to which blockchain and how to operate each one.

NFT Tokens (Non-Fungible Tokens). Represent ownership of unique digital assets – works of art, collectibles, certificates of ownership, and the like. NFTs typically operate on the Ethereum blockchain (though not exclusively) and require a compatible wallet. Valuing them is complicated compared to standard cryptocurrencies – each NFT is unique, and there is no fixed "market price." In inheritance proceedings, professional appraisal is sometimes required for tax purposes and for distribution among heirs.

DeFi Protocol Positions. When the deceased locked cryptocurrency in a Decentralized Finance protocol – for lending, staking, or providing liquidity – the inheritance situation becomes particularly complex. Knowledge of the wallet's Seed Phrase is not sufficient; the heir needs to know which protocol the cryptocurrency is locked in, what actions are required to release it, and sometimes also wait for a certain "unbonding" period before the asset can be realized.

The conclusion is that the preliminary mapping of the deceased's assets is not just "what exists," but also "where it is located, what type of wallet, on which blockchain, and what actions are required for retrieval." An organized instruction document is essential, and without it, even the most dedicated heir may encounter difficulties.

The Tax Framework

Israel has had no estate tax since 1981, and the transfer of crypto assets from the deceased to the heir is not in itself a tax event. However, when the heir seeks to realize the assets, capital gains tax rules apply. Israel Tax Authority Circular 5/2018 regulated the tax treatment of crypto assets, and stipulates, among other things, that the sale of a virtual currency (including conversion between currencies) is a tax event subject to capital gains tax at a rate of 25% (for an individual not engaged in business).

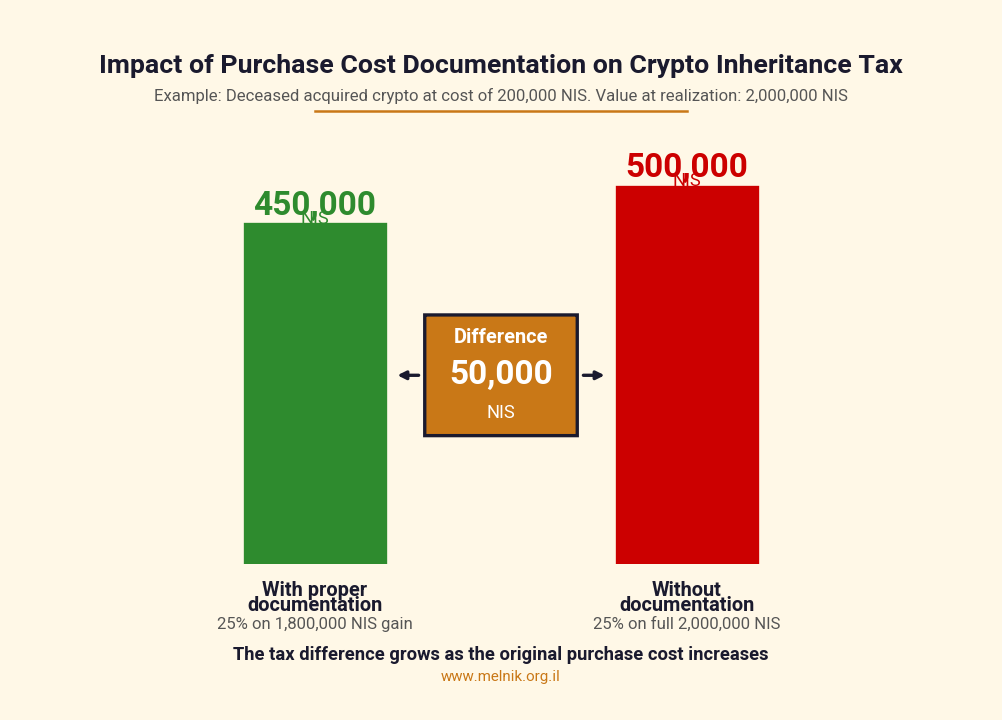

A particularly important point is that the heir "steps into the shoes" of the deceased for tax calculation purposes – a direct result of the classification established in the Kopel ruling. The tax liability will be derived from the difference between the sale price and the original purchase price of the deceased (and not by the value at the time of death). This situation requires the heir to reconstruct the purchase history – sometimes from many years ago. In the absence of appropriate documentation, the Tax Authority may determine a zero purchase price and impose maximum tax liability.

To illustrate the practical significance: assume a deceased who acquired cryptocurrency over the years at a cumulative cost of 200,000 shekels, and passed away when the holdings were worth 2,000,000 shekels. The heir sells the cryptocurrency shortly afterward at the same value. With proper documentation of the purchase cost, the tax liability will be calculated on a gain of 1,800,000 shekels, amounting to approximately 450,000 shekels. Without such documentation, the Tax Authority may determine a zero purchase price, and the tax liability will be calculated on the full 2,000,000 shekels, reaching 500,000 shekels. The difference in tax burden in this example – 50,000 shekels.

In addition, on August 25, 2025, the Israel Tax Authority published a Voluntary Disclosure Procedure (Temporary Order, August 2025), valid until August 31, 2026. This is the first procedure to include explicit reference to digital assets, and allows an heir who has discovered unreported crypto in an estate to regularize the tax liability through a dedicated track, sometimes without criminal exposure. This time window is particularly relevant for heirs who have recently discovered digital assets in an estate, as after August 31, 2026, this dedicated track will no longer be available.

The Digital Content Access Law – What It Does and Does Not Cover

In July 2024, the Digital Content Access Law After a Person's Death, 5784-2024 was enacted, taking effect on July 23, 2025. The law regulates heirs' access to social media accounts, cloud services, and email accounts of the deceased.

However, it is important to emphasize that the law does not apply to crypto assets. Section 3(b) of the law explicitly provides that the mechanism does not apply to digital accounts or content that have economic value, which will continue to be governed by general inheritance law.

The implication: a holder of crypto assets cannot rely on the new law to regulate their transfer to heirs, and must do so through a will and the legal-practical tools that accompany it.

Principles for Planning the Inheritance of Digital Assets

Crypto inheritance planning requires a combination of several elements, which fall within the scope of work of an attorney specializing in inheritance:

First, asset mapping. Since crypto assets do not appear in public records that can be located through a probate order, it is important to prepare a detailed inventory of all wallets, exchange accounts, and types of currencies held. Without such documentation, heirs may not even know that the assets exist. The mapping includes not only a list of the assets but also a specification of each wallet type and the blockchain on which it operates.

Second, arranging practical access. It must be determined how the heirs will receive access to the private keys. Solutions accepted internationally include, among others, splitting the key among several trusted persons using regulated cryptographic methods, using "Multisig" services from specialized companies, or depositing a confidential instruction document in a safe location. The choice between solutions depends on the size of the assets, the level of risk, and the operational complexity desired.

Third, drafting specific clauses in the will. It is advisable to include specific provisions in the will relating to digital assets, including a clear definition of the assets, the appointment of a "digital trustee" responsible for locating and transferring them, and instructions regarding their distribution among heirs. The will itself will not contain the private keys – these will be kept in a separate document, since after the grant of probate the will becomes public.

Fourth, documenting purchase history. As noted above, the heir will need comprehensive documentation of original purchase prices for tax liability calculation. Organized retention of purchase documents, screenshots of transactions, and tax guides from relevant exchanges is an important part of the planning.

The International Trend

In the Western world, legal regulation of the inheritance of digital assets is steadily developing. In the United States, the Revised Uniform Fiduciary Access to Digital Assets Act (RUFADAA) has been adopted in 46 states and the District of Columbia, and in the United Kingdom the Property (Digital Assets etc) Act 2025 was enacted on December 2, 2025 – the first law to recognize digital assets as a separate category of property.

In the European Union, the MiCA regulation (Markets in Crypto-Assets) came into force on December 30, 2024, regulating the crypto market at the European level, including inheritance-related aspects. Israel, as of now, has not yet enacted dedicated legislation for digital assets, although a memorandum from November 2024 anticipates legislative development in the field in the coming years.

Conclusion

Inheritance of crypto and other digital assets is a relatively young field, but one that is gaining importance with the expansion of asset holdings among the Israeli public. While the legal framework in Israel clearly stipulates that these assets pass to heirs in the same way as other assets, practical implementation of the inheritance requires advance and specialized planning – both in the legal aspect and in the technical aspect. The variation between different asset types – cold wallets, hot wallets, exchange accounts, different blockchains, NFTs, and DeFi positions – increases the importance of tailored and individualized planning.

Anyone holding crypto assets in significant volume, or anticipating acquiring such assets in the future, would do well to consult an attorney familiar with the field when drafting or updating their will, and to ensure that their digital assets are included within the overall framework of estate planning. Advance planning can prevent unfortunate situations in which valuable assets are lost forever due to inaccessibility, or in which heirs are required to incur complex legal expenses to realize their rights.

The information in this article is general and informational, and should not be considered specific legal advice. Each case requires individual examination.